From 1 April 2017 HMRC introduced changes to the flat VAT rate scheme.

The flat rate scheme was introduced to reduce the administrative burden of small businesses. Under the scheme the business can apply a flat rate percentage to its turnover instead of having to account for VAT on all its sales and purchases. This flat rate percentage is determined on the type of industry that the business is in.

Businesses can opt into the scheme if their turnover is under £150,000 per year. They can remain in the scheme until their turnover exceeds £230,000 per annum.

What is changing?

HMRC believed that the scheme had been open to abuse with some businesses registering for the flat rate scheme as a way of paying less VAT.

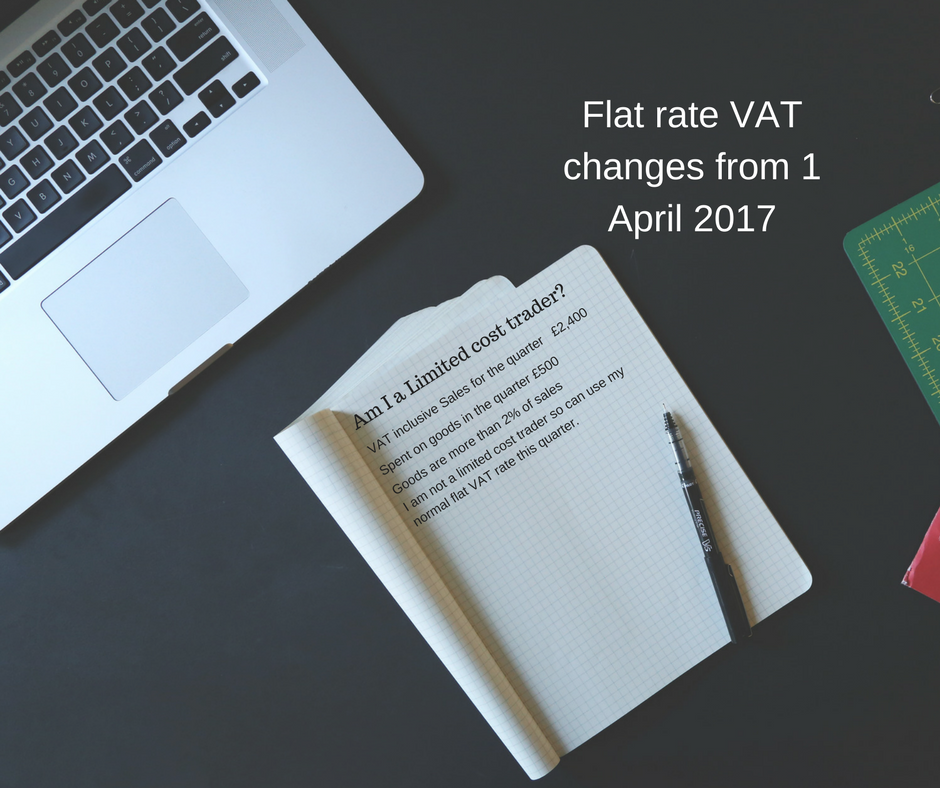

Therefore from 1 April 2017 a new percentage (16.5%) was introduced for ‘limited cost traders’.

This type of trader is defined as one that spends less than 2% of its VAT inclusive turnover on goods in the accounting period. If a business’ VAT inclusive expenditure on goods is more than 2% but less than £1,000 per year they will also be caught under the ‘limited costs trader’ rules.

When looking at goods they must be:

- Used exclusively for the business. Therefore, any goods which have any personal use cannot be included.

- Cannot be capital items, food or drink, vehicles, vehicle parts and fuel.

Note that a business needs to look at their purchase of goods not services.

How will this affect my business?

Each time your business completes a VAT return it will need to check whether it is a limited cost trader. If it is a limited cost trader for that quarter, it should use the 16.5% flat rate. If it is not a limited cost trader it should use the normal flat rate percentage for its industry.

A business can still get a 1% discount in the first year of using the flat rate scheme.

I am on the flat rate scheme and am now classed as a limited cost trader. What can I do?

You could stay on the flat rate scheme and pay more VAT each quarter. The benefit of doing this is that it might reduce your admin burden.

Alternatively, you could leave the flat rate scheme. If your annual turnover is less than the VAT registration threshold (currently £85,000) you can completely deregister for VAT or use the standard VAT scheme.

If your turnover is over the VAT threshold of £85,000 you can opt out of the flat rate scheme and use standard VAT accounting instead.

To leave the flat rate scheme you will need to notify HMRC either by email or in writing.

If you leave the flat rate scheme you cannot rejoin it for another 12 months.

Example

Valerie is an architect and she has an annual VAT inclusive turnover of £108,000. Under the flat rate scheme she qualifies for a flat rate percentage of 14.5%. She would therefore have an annual VAT liability of £15,660.

Her annual expenditure on goods is only £2,000 spread evenly throughout the year which is less than 2% of her VAT inclusive turnover so she will be classed as a Limited cost trader. Her annual VAT liability will therefore increase to £17,820 an increase of £2,160 per annum.

Her turnover is over £85,000 per annum so she has to remain registered for VAT. If she leaves the flat rate scheme and moves to the standard accounting scheme the VAT due on her sales will be £18,000. Therefore, if the VAT on her purchases is more than £180 (£18,000 less £17,820) she will be better off by leaving the flat rate scheme.

If you are unsure about whether you should be in the flat rate scheme you should speak to an accountant. If you give us a call on 01452 260960 we will be happy to assist you.

Links:

Gov.uk – Limited cost trader calculator

{kind=link}